The canned beer flavor landscape in 2026 is splitting into two distinct growth vectors that are, at their intersection, creating the most commercially interesting OEM opportunity in the entire category. On one side: the global tropical fruit wave, anchored by peach, mango, and passionfruit, which is driving the fruit beer market toward USD 520.8 million by 2033 at a 4.8% CAGR.

The canned beer flavor landscape in 2026 is splitting into two distinct growth vectors that are, at their intersection, creating the most commercially interesting OEM opportunity in the entire category. On one side: the global tropical fruit wave, anchored by peach, mango, and passionfruit, which is driving the fruit beer market toward USD 520.8 million by 2033 at a 4.8% CAGR. On the other side: the Chinese tea heritage boom — specifically, Longjing, jasmine, and oolong craft beers — which erupted onto China's domestic market in 2024 and is now crossing into export OEM demand globally. For beverage brands and importers deciding where to invest their next OEM order, mapping these two trends and their intersection is the most valuable analysis you can do in the first half of 2026.

Key Takeaways

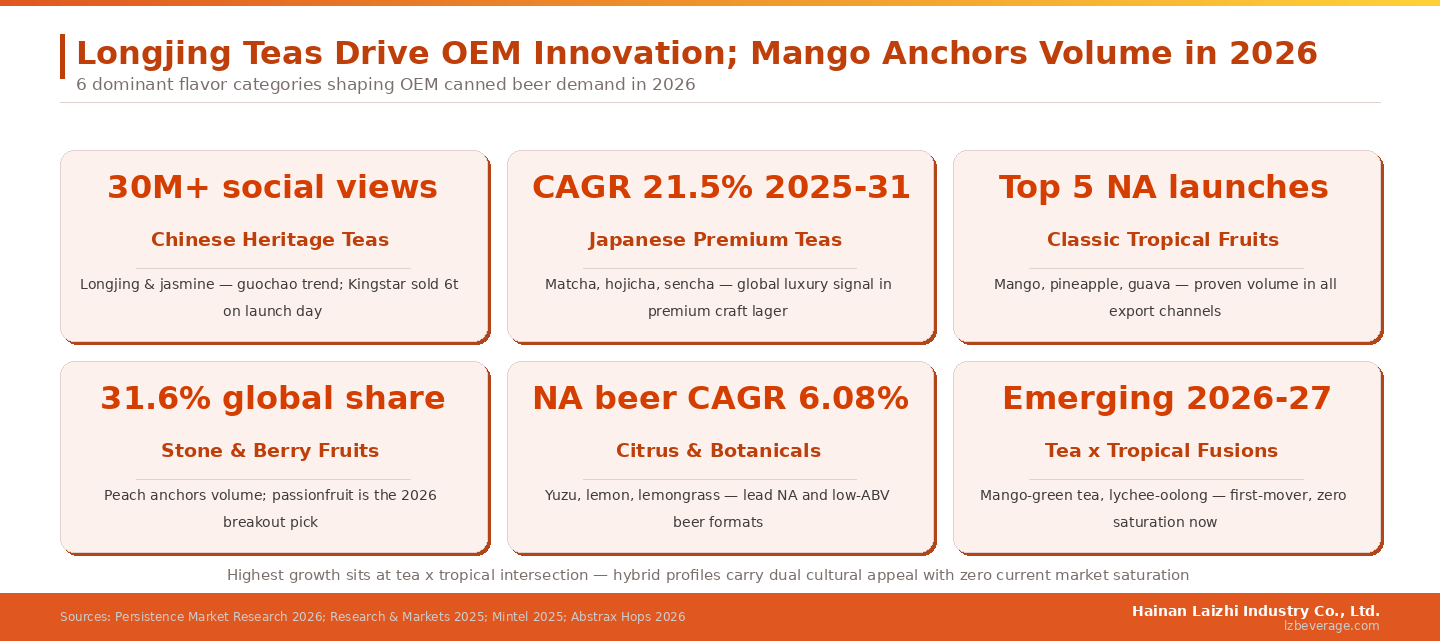

- China's Longjing tea beer trend is validated and exportable — short-video content about tea beer accumulated over 30 million views on Chinese social media in 2024–2025, and the format is now attracting international curiosity from Asian diaspora markets and specialty beverage buyers.

- Peach remains the global volume leader with 31.6% of fruit beer market share, while passionfruit holds the clearest first-mover OEM advantage as an "emerging with stable growth" category in 2026.

- Tea × tropical fruit hybrids represent the 2026–2027 first-mover window — mango-green tea, lychee-oolong, and pandan-jasmine combinations are not yet saturated in any major export market.

- Longjing wheat beer has proven real consumer demand in China — validated by on-premise sell-through data from Beijing craft beer bars and e-commerce livestreaming virality.

- The "guochao" (national pride) trend amplifies Chinese tea beer's brand potential — products with authentic regional tea provenance (West Lake Longjing, Anxi Tieguanyin, Xishuangbanna Pu'er) carry cultural equity that generic flavors cannot replicate.

The Two Megatrends Reshaping Canned Beer Flavor in 2026

Megatrend 1: The Global Tropical Fruit Wave

The tropical fruit flavor wave in canned beer is not a new trend — it is a maturing, deepening one. What began as an experimental craft brewing technique (adding fruit purees to sours and wheat ales) has graduated into a mainstream commercial category. According to Beer Connoisseur's analysis of Persistence Market Research data, peach holds 31.6% of the global fruit beer market — a dominant position built on universal consumer appeal and production reliability. Mango has crossed from trend to staple, appearing in IPAs, wheat ales, Berliner Weisses, and lagers across virtually every geography. And as the 2026 Craft Brewers Conference demonstrated, the next wave of tropical novelty — marionberry, passionfruit, Sicilian lemon — is already visible in the craft brewing community's purchase behavior.

Megatrend 2: Chinese Tea Heritage Beer (茶啤 / Chá Pí)

The Chinese tea beer phenomenon is younger and faster. In August 2024, Henan Kingstar Beer launched a craft beer infused with Xinyang Maojian tea — a premium green tea from Henan province — and sold six tonnes on its first day of livestreaming, topping beer category sales across platforms according to Vino Joy's industry report. Short-video content about tea beer accumulated over 30 million views on Chinese social media in 2024–2025. This was not a random viral moment — it validated a structural shift: young Chinese consumers who might not drink traditional beer are open to tea beer because it bridges their most familiar beverage (tea) with the social drinking occasion.

As CKGSB Knowledge's 2026 analysis of China's craft beer industry notes, Longjing-flavored and lychee-flavored beers are now available in mainstream Chinese supermarkets as "fresh craft beer" formats — a sign that the category has moved beyond niche craft bar validation into commercial distribution. For OEM brands, this means the formulation templates and consumer validation work has been done. The opportunity is to take this proven concept to international export markets where Chinese tea beer remains genuinely novel.

The Full 2026 Flavor Spectrum: Six Categories OEM Buyers Need to Map

Category 1: Chinese Heritage Teas — The Guochao OEM Opportunity

Longjing (Dragon Well), jasmine, Tieguanyin (Iron Goddess of Mercy), Pu'er, Xinyang Maojian — each of these represents not just a flavor profile but a cultural narrative. The guochao (national chic/national pride) trend among Chinese consumers aged 18–35 has created a premium market for products that authentically reference Chinese cultural heritage. A Longjing wheat beer made with single-origin West Lake tea — brewed at a Hainan facility with genuine access to Chinese tea supply chains — carries a provenance story that resonates deeply in Chinese domestic markets and in Asian diaspora markets globally. Explore Laizhi Beverage's tea product expertise as a foundation for understanding how Chinese tea heritage translates into commercial beverage production.

According to Daxue Consulting's 2026 China beer market analysis, tea-infused beer has gained significant commercial traction by mixing jasmine or Longjing tea with standard ales — and social media platform Xiaohongshu features over 30,000 posts discussing which tea beer tastes best. This is consumer-generated demand validation at scale.

Category 2: Japanese Premium Teas — The Export Craft Premium

Matcha, hojicha, and sencha occupy a different brand position from Chinese heritage teas. They carry a global luxury signal — matcha in particular has penetrated Western markets through specialty coffee shops and premium food products, meaning international consumers outside Japan already have a matcha taste reference. For OEM brands targeting European specialty retailers, North American craft beer stores, or Middle Eastern premium hospitality, a matcha-infused pale ale or hojicha brown ale carries a legitimizing flavor signal that Chinese heritage teas — while growing — do not yet have in those same markets. The global tea beer category is forecast to grow at 21.5% CAGR through 2031, with green tea identified as the fastest-growing tea type within the segment.

Category 3: Classic Tropical — The Export Volume Engine

No strategic review of 2026 canned beer flavors is complete without acknowledging that peach, mango, and pineapple remain the volume anchors of the entire fruit beer category. For OEM buyers who need reliable sell-through and export market acceptance, these are the core SKUs. Mango is described by Abstrax Hops' 2026 flavor intelligence report as having crossed from trend to "beverage staple" — it is not a trend to ride, it is a category standard to be in. For market entry, a mango wheat ale or peach lager in 330ml cans is the lowest-risk foundation for an OEM craft beer portfolio. Build differentiation on top of this foundation, not instead of it.

Category 4: Stone and Berry Fruits — The Craft Credibility Range

Peach's 31.6% market share makes it the anchor; passionfruit's "emerging with stable growth" classification from Mintel's Flavourscape AI makes it the upside opportunity. Marionberry's dominance of the 2026 Craft Brewers Conference floor conversation signals that the market is ready for regionally specific berry varieties that carry novelty and craft credibility simultaneously. For OEM buyers building a craft beer portfolio, one classic (peach or raspberry) and one emerging (passionfruit or marionberry) in the same collection creates a credible range signal: the classic generates volume, the emerging generates press and social attention.

Category 5: Citrus and Botanicals — The NA and Low-ABV Growth Engine

Lemon, grapefruit, yuzu, and lemongrass are doing specific work in the non-alcoholic and low-ABV beer segment — the category growing at 6.08% CAGR in Asia Pacific through 2033. Citrus flavors compensate for the absence of ethanol warmth in NA beer, providing refreshing acidity that makes the drinking experience satisfying without alcohol. For OEM brands looking to participate in the NA beer trend without the formulation complexity of de-alcoholization, a low-ABV (under 3%) lemon or yuzu wheat beer occupies a similar brand space with simpler production requirements.

Category 6: Tea × Tropical Fusions — The 2026–2027 First-Mover Window

This is where the two megatrends converge — and where the most strategically interesting OEM opportunity in canned beer currently sits. Mango-green tea beer. Lychee-oolong ale. Pandan-jasmine wheat beer. These hybrid profiles do not exist in the crowded center of any market yet. They appeal to consumers at two entry points simultaneously: Asian cultural identity (through the tea component) and global tropical flavor familiarity (through the fruit component). Brands that launch into this category in late 2026 or early 2027 are genuinely early, given the current state of commercial SKU availability in major export markets. Contact Laizhi Beverage to explore custom formulation development in this category — the combination of Chinese tea expertise and tropical fruit OEM capability makes this a natural fit for Laizhi's production platform.

OEM Sourcing Strategy: Which Flavor to Launch First

The Conviction-vs.-Volume Decision

Every OEM buyer faces the same core decision: launch a proven, high-volume flavor (peach, mango) and compete on production quality and price, or launch a differentiated, emerging flavor (passionfruit, Longjing tea hybrid) and compete on novelty and brand positioning. Neither answer is wrong — the right choice depends entirely on your distribution channel and competitive context. For convenience channel buyers (7-Eleven, supermarket chains, food service distributors), proven flavors at reliable supply quality will always outperform novelty. For specialty retail buyers, craft beer importers, and premium online channels, differentiation is the primary purchase driver — and Longjing wheat beer, matcha pale ale, or passionfruit sour will generate more buyer attention than a technically excellent generic peach lager.

| Flavor Category |

Best Channel |

OEM Risk Level |

Differentiation Potential |

2026 Launch Timing |

| Peach / Mango |

Convenience, supermarket |

Low |

Low — highly competitive |

Any time — evergreen |

| Passionfruit / Marionberry |

Specialty retail, craft |

Medium |

High — early in growth curve |

H2 2026 — now is early |

| Longjing / Jasmine Tea Beer |

Asian specialty, premium online |

Medium |

Very High — proven in China, novel globally |

Now — export window open |

| Tea × Tropical Fusions |

Premium specialty, hospitality |

Medium-High |

Maximum — no competition yet |

2026-2027 — first-mover window |

Frequently Asked Questions

Is Longjing tea beer only for Chinese markets?

No — and this is one of the key OEM insights for 2026. While Longjing tea beer originated in and is proven in China, its export potential extends to Asian diaspora communities in North America, Europe, and Australia; specialty Asian grocery retailers in those same markets; and premium craft beer buyers who are actively seeking novel cultural flavor concepts. The provenance story ("brewed with West Lake Longjing, one of China's ten famous teas") is compelling in any premium specialty retail context.

What is the difference between a "tea beer" and a "tea-flavored beer"?

A "tea beer" typically uses actual tea leaves or tea concentrate at some stage of production — either in the brewing process, post-fermentation, or as a cold-brew addition at packaging. A "tea-flavored beer" may use natural or artificial tea flavor extracts. The distinction matters for labeling and brand positioning: "brewed with Longjing tea" is a significantly stronger premium claim than "tea-flavored," and should only be made when the production method actually involves real tea. Most credible OEM producers offer both options at different price points.

Which tropical fruit beer flavor will have the most growth in 2026–2027?

Passionfruit offers the clearest growth trajectory among tropical flavors that have not yet saturated the market. Mintel's Flavourscape AI classifies it as "emerging with stable growth" as of early 2026 — which is precisely the stage at which OEM brands benefit most from launching. Mango and peach are proven volume categories; passionfruit is where the premium differentiation premium exists right now.

Can I launch both a Chinese tea beer and a tropical fruit beer from the same OEM manufacturer?

Yes, and doing so from a single OEM source is more efficient than sourcing from two suppliers. A manufacturer with formulation flexibility across both tea infusion and fruit flavor integration — and HACCP-certified production for both — can deliver both SKUs from the same facility, simplifying logistics, export documentation, and quality control. Browse Laizhi Beverage's beer OEM options and consider how the tea expertise in the broader product range applies to tea beer formulation development.

How do I protect my Longjing tea beer recipe from being copied by competitors?

Recipe protection in OEM relationships relies on contractual confidentiality, not patent law. A well-structured OEM manufacturing agreement should include confidentiality clauses covering the formulation, a market or channel exclusivity clause preventing the same formula from being sold to your direct competitors, and a clear IP ownership statement confirming that any custom formula developed jointly belongs to your brand. Have these terms reviewed by a trade lawyer with experience in cross-border OEM agreements before production begins.