The canned-versus-bottled debate has been settled for most commercial beverage segments, but for craft beer OEM brands — especially those targeting export markets in Southeast Asia, the Middle East, Africa, and Europe — the choice between aluminum cans and glass bottles carries consequences that extend beyond aesthetics. It affects flavor stability during transit, carbon footprint across the supply chain, shelf presence in retail, and the economics of your first and subsequent production runs.

The canned-versus-bottled debate has been settled for most commercial beverage segments, but for craft beer OEM brands — especially those targeting export markets in Southeast Asia, the Middle East, Africa, and Europe — the choice between aluminum cans and glass bottles carries consequences that extend beyond aesthetics. It affects flavor stability during transit, carbon footprint across the supply chain, shelf presence in retail, and the economics of your first and subsequent production runs. According to Mordor Intelligence, cans captured 54.44% of the global craft beer packaging market in 2025, reflecting a decisive shift that took less than a decade to complete. But understanding why that shift happened — and whether it applies to your brand — requires looking at the data across five dimensions that OEM buyers care about most.

Key Takeaways

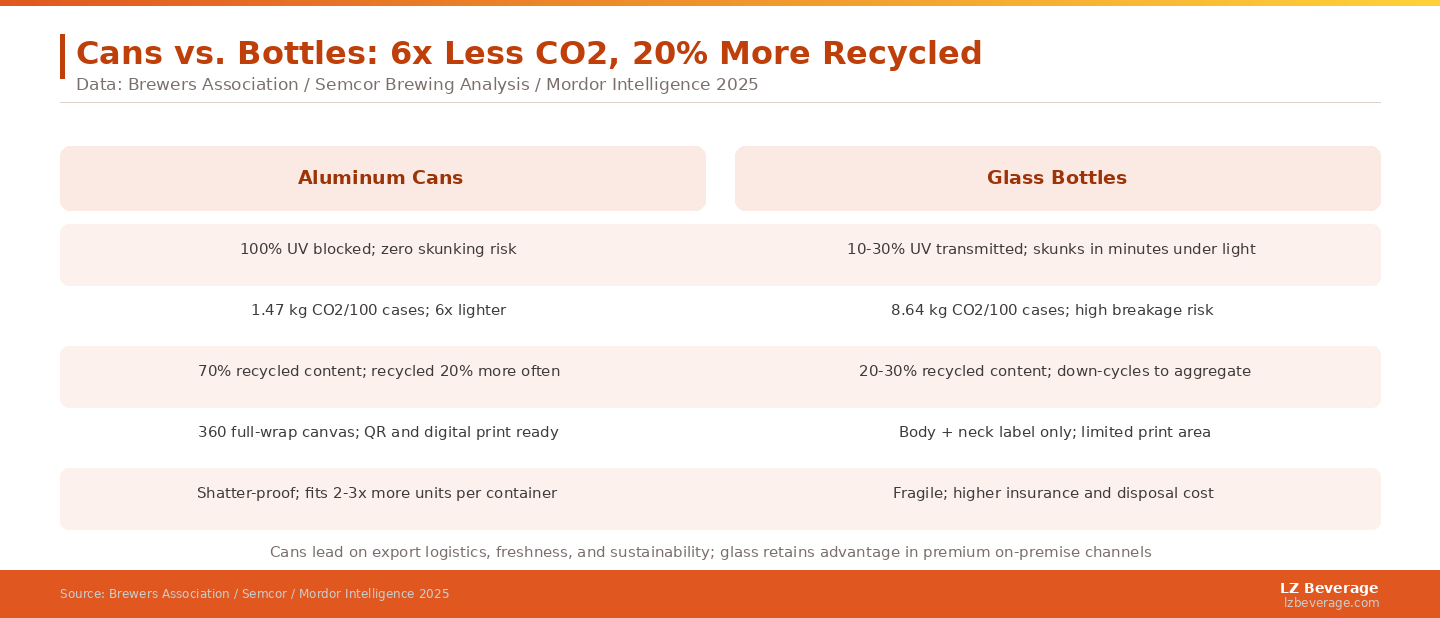

- Cans block 100% of UV light; brown glass transmits 10–30% — making canned craft beer meaningfully more resistant to light-induced flavor degradation during storage and transport.

- Transport CO₂ emissions for canned beer are approximately 6x lower than bottled beer per 100 cases shipped, a significant factor for export-focused OEM brands managing landed cost.

- Aluminum cans contain ~70% recycled content versus 20–30% for glass bottles, and consumers recycle cans at a rate 20% higher than glass.

- Bottles retain a perception advantage in premium on-trade settings — hotel bars, fine dining, and hospitality channels — where the ritual of uncapping matters as much as the beer inside.

- For first-time OEM export orders, cans reduce supply chain risk through shatter-proof logistics and 2–3x higher stacking density per container.

The Technical Case: How Packaging Affects Beer Quality

Light Protection — Where Cans Win Definitively

UV light is the primary enemy of hop-forward craft beers. When UV rays interact with hop compounds in beer, they trigger a photochemical reaction that produces 3-methyl-2-butene-1-thiol — the compound responsible for the "skunky" aroma that marks a lightstruck beer. Brown glass bottles, which are the standard for quality craft beer packaging, transmit roughly 10–30% of UV wavelengths. Clear and green glass bottles perform significantly worse. Aluminum cans, by contrast, block 100% of all light wavelengths — there is no UV transmission through the can wall at any point in the supply chain. For OEM craft brands shipping to markets where cold chain management is inconsistent, or where product may spend time in warm, illuminated storage conditions, the can's complete light barrier is a quality protection that glass simply cannot match.

The Brewers Association's packaging trend analysis notes that the perception gap between cans and bottles on quality has narrowed significantly as craft brewers have shifted more volume into aluminum — partly because consumers drinking canned craft IPA are experiencing fresher beer than they were getting from bottles under comparable storage conditions. This quality-driven evidence has been a stronger driver of the can share gain than marketing alone.

Oxygen Ingress — More Nuanced Than It Appears

Oxygen management is the second critical freshness dimension. A well-seamed aluminum can creates a hermetic seal with virtually zero external oxygen ingress after filling, whereas standard crown bottle caps permit trace oxygen diffusion through the gasket material over time. However, at the point of packaging, cans often have slightly higher headspace oxygen than bottles due to how they are filled on high-speed lines. The net effect over a full shelf life is that cans typically outperform bottles on oxidation stability by week three to four of storage — a meaningful window for export products with 6–12 month shelf life requirements. For OEM buyers purchasing products destined for markets four to eight weeks' shipping time away, this is a material quality consideration, not a theoretical one.

The Export Logistics Case: Why OEM Brands Favor Cans

Transport Efficiency and Cost

The shipping economics of cans versus bottles are not close. According to brewing industry analysis cited by Semcor, a 100-case shipment of canned beer by truck produces approximately 1.47 kg of CO₂ compared to 8.64 kg for the glass bottle equivalent — a six-fold difference driven almost entirely by the weight differential between aluminum and glass. In freight economics, lighter product means more units per container load, lower per-unit freight cost, and reduced fuel consumption across the entire distribution chain. For an OEM brand shipping a 20-foot container from China to a Southeast Asian or Middle Eastern importer, the freight cost difference between a can and bottle product can amount to thousands of dollars per container — money that either improves margin or reduces retail price in the destination market.

Durability in Transit

Glass breakage is an invisible cost that first-time OEM buyers often underestimate. Over a multi-week ocean freight journey — with container stacking, port handling, and last-mile delivery at the destination — glass bottles are exposed to dozens of impact events that cans absorb without consequence. A conservative breakage rate of 1–2% on bottled product means 200–400 broken units per 20,000-unit container, plus secondary damage to adjacent bottles from leakage. Aluminum cans are shatter-proof under normal handling conditions. For OEM brands building their first distribution relationship in a new market, a shipment that arrives fully intact is a relationship-building event. Reviewing a factory's quality control and production infrastructure documentation before the first order is standard due diligence for first-time buyers; a shipment with broken bottles is a dispute.

The Brand Case: When Each Format Wins

When Cans Are the Right Choice

The aluminum can's 360-degree full-wrap canvas is a brand communication advantage that bottles cannot replicate. The entire exterior surface of a can is available for artwork, typography, QR codes, and promotional messaging — versus the body label and neck label area of a bottle, which covers roughly 30–40% of the surface. For brands launching in competitive retail environments where shelf standout drives trial, the can's visual real estate is a meaningful asset. Custom can label and artwork options for OEM beer production allow brands to create visual identities that compete with established names at eye level. Cans are also the correct format for hop-forward styles (IPAs, pale ales, hazys), outdoor consumption occasions (music festivals, sports venues, beach and outdoor retail), and e-commerce or direct-to-consumer shipping where package integrity during last-mile delivery matters.

When Bottles Remain the Right Choice

Glass bottles retain genuine advantages in specific commercial contexts. For craft beer brands targeting hotel bars, fine dining restaurants, or premium retail where the theater of serving — uncapping a bottle, pouring into a specific glass, presenting the label — is part of the value proposition, bottles communicate premium quality signals that many hospitality buyers still prefer. According to Market Data Forecast, 65% of millennials globally are willing to pay a premium for craft beer — and in premium on-trade channels, the product's container is part of what they are paying for. Bottle formats are also advantageous for barrel-aged or cellar-worthy craft styles where extended bottle conditioning is part of the brewing philosophy, and for Belgian-style ales with traditional cork-and-cage presentation.

The Sustainability Case: Cans Lead on Measurable Metrics

The environmental comparison between aluminum cans and glass bottles favors cans across most measurable dimensions. Aluminum cans contain approximately 70% recycled content at the point of manufacture, versus 20–30% for glass bottles, according to brewery operations data. Post-consumer, consumers recycle cans at a rate approximately 20% higher than glass, and aluminum can be recycled indefinitely without downgrading the material — a property that glass does not share (recycled glass typically downcycles to aggregate rather than new glass bottles). These metrics are increasingly relevant to OEM brands selling into European and North American markets where retailer and distributor ESG scorecards are beginning to influence supplier selection decisions. Learn more about sustainable packaging considerations for OEM beverage production and how they affect your brand's positioning in environmentally conscious markets.

Making the Decision: A Practical OEM Framework

The packaging format decision for a craft beer OEM brand should be driven by three questions in sequence. First, what is the primary consumption occasion for your product in the target market — on-trade premium, off-trade retail, or outdoor/event? Second, what are the import regulations and labeling requirements for your target market, and do either format present regulatory complications? Third, what is your first-order volume and what format minimizes your capital risk at that volume? If the answers point toward outdoor or retail consumption, export logistics, and flexible volume management, cans are the correct choice. If the answers point toward premium hospitality or aged specialty styles with established distribution in high-end on-trade, bottles may justify the higher logistics cost and breakage risk. According to industry projections, the global craft beer market is expected to grow from USD 129 billion in 2025 to USD 360 billion by 2035 at 10.8% CAGR — brands that enter in 2025–2026 with the right format decision will be better positioned to capture this decade's growth window than those who delay while deliberating. Contact an OEM production specialist to discuss format options for your specific market and style profile.

Frequently Asked Questions

Does craft beer taste different in cans versus bottles?

In controlled blind taste tests, most drinkers cannot reliably distinguish canned from bottled beer when both are fresh. Any perceived taste difference is primarily psychological — the expectation that glass means premium — rather than a genuine chemical difference. Modern aluminum cans are lined with a food-safe polymer coating that prevents any interaction between the beer and the aluminum wall. For hop-forward styles, fresh cans consistently outperform bottles that have experienced any UV exposure during storage or transit, which is a real-world advantage rather than a theoretical one.

Which format is better for craft beer in export markets?

For most export markets — particularly those in Southeast Asia, the Middle East, Africa, and emerging markets generally — cans are the superior format. They survive long-haul shipping without breakage risk, are more freight-efficient, and provide complete flavor protection during the transit period. The exception is premium hospitality in established markets (Western Europe, Japan, Australia) where bottled craft beer commands higher on-trade pricing and is preferred by venue buyers. Many OEM brands resolve this by launching in cans for off-trade retail entry and adding a bottle format for on-trade premium placement in a second production run after market validation.

Is it more expensive to produce craft beer in cans or bottles at an OEM factory?

The unit economics are approximately comparable at commercial scale, but differ in important ways. Bottles typically have lower setup costs and lower order minimums because bottling line changeovers are faster and bottle labeling requires less print-run commitment than lithographed cans. The Business Research Company notes that 9,796 U.S. craft breweries operated in 2024, the majority offering bottles as their entry format. Cans require higher minimum can order quantities — typically 50,000+ units for printed cans — but provide ongoing freight cost savings that often offset the higher initial setup within two to three shipments. For OEM brands planning multi-year market development, cans typically deliver better total cost of ownership despite the higher entry barrier. Market Research Future projects the craft beer market to reach USD 391 billion by 2035, suggesting the investment in establishing the right format now will yield returns across a sustained growth period.