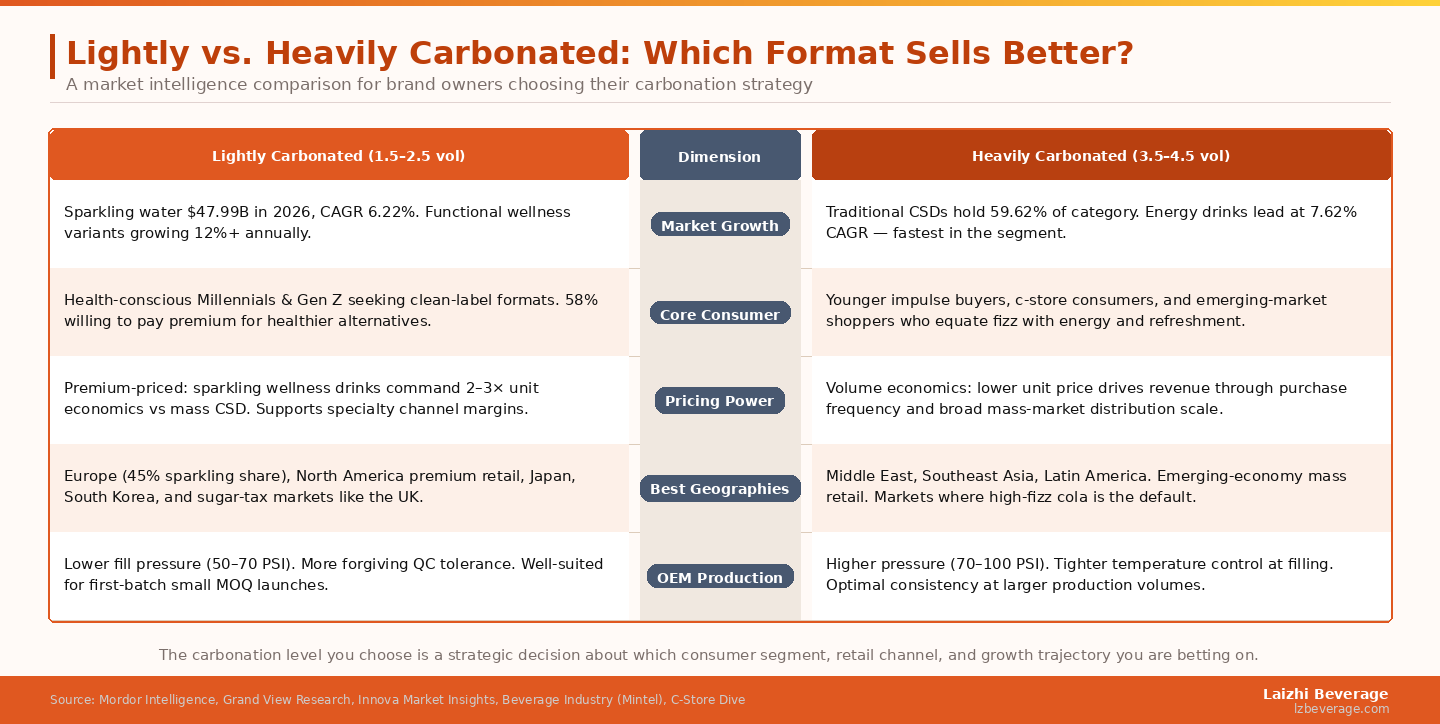

The carbonated beverage market sits at a fascinating inflection point in 2026. On one side, traditional heavily carbonated sodas and energy drinks continue to generate enormous volume — the overall market is estimated at USD 589.66 billion in 2026, according to Mordor Intelligence, with carbonated sports and energy drinks growing at a 7.62% CAGR.

The carbonated beverage market sits at a fascinating inflection point in 2026. On one side, traditional heavily carbonated sodas and energy drinks continue to generate enormous volume — the overall market is estimated at USD 589.66 billion in 2026, according to Mordor Intelligence, with carbonated sports and energy drinks growing at a 7.62% CAGR. On the other side, lightly carbonated sparkling waters have emerged as one of the beverage industry's most dynamic growth stories, with the global sparkling water category projected at USD 47.99 billion in 2026 and growing at 6.22% CAGR through 2031. For brand owners evaluating their next product launch, the central question isn't whether carbonation sells — it's which level of carbonation sells better for their specific target consumer, channel, and geography. This article provides a structured comparison to help you make that decision.

Key Takeaways

- Lightly carbonated formats (1.5–2.5 vol CO2) command higher price premiums and lead in wellness and functional beverage positioning, especially among Millennial and Gen Z consumers.

- Heavily carbonated formats (3.5–4.5 vol CO2) drive higher volume, dominate c-store and mass retail channels, and generate stronger impulse purchase patterns.

- Geography matters: European consumers skew toward light carbonation and mineral water; the Middle East, Southeast Asia, and Latin America favor high-carbonation cola and energy drink styles.

- Neither format is universally "better" — the right choice depends on your distribution channel, retail margin strategy, and the demographic you are targeting.

Defining the Two Formats

What "Lightly Carbonated" Means in Practice

In industry terminology, lightly carbonated beverages typically fall in the 1.5–2.5 vol/vol CO2 range. This includes most still sparkling waters, lightly sparkling teas, botanical sodas, and wellness-oriented carbonated RTDs. At this level, the effervescence is perceptible but gentle — a soft, refreshing tingle rather than an aggressive bite. As the University of Florida IFAS Extension's beverage carbonation guide documents, many fruit-flavored and wellness beverages are intentionally formulated in the 1.0–2.5 vol range to deliver carbonation's sensory benefits without overwhelming the delicate flavor notes that define these products.

What "Heavily Carbonated" Means in Practice

Heavily carbonated beverages span the 3.5–4.5 vol/vol range for most commercial formats, with some craft sodas approaching 5.0 vol in specialized applications. According to ScienceDirect's overview of carbonation science, this classification covers colas and tonics (3.5+ vol), which need higher CO2 to counterbalance sweetness and create the sharp, mouth-filling sensation that consumers associate with energy and indulgence. The carbonation at this level is immediately noticeable — it defines the drinking experience rather than simply enhancing it.

Market Growth: Who's Winning in Volume and Value?

The Volume Story: Heavy Carbonation Still Dominates

By absolute volume and dollar sales, heavily carbonated formats remain the dominant force. Traditional carbonated soft drinks held 59.62% of the carbonated beverages market in 2025. The energy drink segment, which primarily uses high-carbonation formats to deliver its signature mouthfeel, has reached an all-time high in market share — in convenience stores in the US, C-Store Dive reports energy drinks exceeded $16 billion in sales in the 12 months to October 2025, with unit sales growing 8%. For brand owners targeting c-store placement, high-volume impulse purchase channels, or sports and performance demographics, high carbonation remains the dominant format.

The Growth Story: Light Carbonation Has the Momentum

Growth rate tells a different story. The sparkling water market — essentially the lightly carbonated segment — is one of the fastest-scaling categories in beverages. This shift is primarily driven by health-conscious consumers, particularly Millennials and Gen Z. According to Innova Market Insights, 78% of US consumers drink carbonated beverages at least once a week, with roughly 30% of Gen Z and Millennials actively increasing their consumption. Crucially, the growth concentration is in lighter, cleaner formats — sparkling water, functional sparkling drinks, and lightly carbonated teas — rather than traditional colas or high-energy sodas.

Industry analysis from Beverage Industry magazine puts the CSD market size at $55.2 billion in 2024, up 5.1%, but notes that the growth is increasingly driven by premium, functional, and reduced-sugar formats that skew toward gentler carbonation levels. The high-carbonation, high-sugar mass CSD segment is growing more slowly than the category average.

Consumer Demographics: Who Buys Each Format?

Lightly Carbonated: Millennials, Gen Z, and the Wellness Consumer

Lightly carbonated beverages command disproportionate interest among younger, higher-income, and health-conscious consumers. The key drivers are clear: these consumers are reducing sugar intake, seeking "clean label" formulations with recognizable ingredients, and using sparkling beverages as a substitute for both still water and traditional sodas. The wellness positioning of a 2.0 vol/vol sparkling green tea or a 1.8 vol/vol prebiotic soda aligns perfectly with the values this demographic applies to every purchase decision. This creates a favorable pricing dynamic — as Beverage Industry's Mintel research notes, about 58% of consumers are willing to pay more for healthier alternatives, and 32% express active interest in functional CSD innovations.

For brand owners building for the premium channel — specialty grocery, direct-to-consumer, subscription boxes, health food retail — lightly carbonated formats command stronger pricing power and margin. A functional sparkling tea or prebiotic-infused sparkling water can retail at 2–3× the unit price of a comparable mass-market cola, supporting healthier brand economics. This is an important consideration for OEM brands planning to launch in the tea or sparkling RTD category.

Heavily Carbonated: Gen Z Energy, Mass Market, and Emerging Economies

High-carbonation formats retain strong loyalty among two distinct populations: Gen Z consumers who specifically seek energy drinks and bold soda experiences (where carbonation intensity is itself a positive signal), and mass-market consumers in emerging economies where affordability, availability, and established flavor preferences favor cola-style and high-carbonation drinks. The energy drink segment is particularly revealing: C-Store Dive's analysis notes that younger consumers are "much more likely than their older peers to select energy drinks because they enjoy their carbonation" — the aggressive fizz is a feature, not a drawback.

Heavily carbonated formats also win on impulse purchase frequency. The sharp, immediate sensory experience of opening a cold, highly carbonated can creates a strong conditioned purchase pattern that drives repeat buying in convenience channels. This makes high-carbonation formats a natural fit for brands targeting frequency-based revenue rather than premium margin. Developing a custom energy drink for an OEM brand launch captures both the growth trajectory of the segment and the impulse purchase dynamic that makes convenience channel placement profitable.

Geographic Markets: Where Each Format Wins

Europe: The Home of Light Carbonation

European consumers have historically preferred lighter sparkling waters — especially in Germany, Italy, France, and the UK, where naturally carbonated mineral waters are cultural staples. Europe held approximately 45% of the global sparkling water market in 2025 and continues to lead in per capita consumption of premium, lightly carbonated waters. Brands entering European export markets face a consumer landscape where "light carbonation" signals quality and premium authenticity. The UK's Soft Drinks Industry Levy has further accelerated the shift away from high-sugar, heavily carbonated sodas, with industry data showing a 40% reduction in sugar content across affected products after the levy's introduction.

Middle East, Southeast Asia, and Latin America: High-Carbonation Territory

Outside Europe and the coasts of North America, heavily carbonated formats maintain much stronger consumer preference. In the Middle East, cola-style heavily carbonated drinks remain the dominant soft drink choice — with added growth from the functional energy drink segment driven by a young, highly urban population. Southeast Asia and Latin America are experiencing rapid growth in carbonated beverage consumption overall, driven by urbanization, rising disposable incomes, and the expansion of modern retail. In these markets, a lightly sparkling wellness drink often faces a cultural familiarity challenge — consumers expect a more pronounced fizz. For brands building primarily for export to these geographies, a starting carbonation target of 3.0–3.5 vol/vol gives them a product that feels familiar and refreshing to the target consumer.

The Middle Path: 2.5–3.0 Vol as a Cross-Market Sweet Spot

A growing number of brands are targeting the 2.5–3.0 vol/vol "moderate carbonation" range precisely because it straddles both demographic and geographic expectations. This range is light enough to position as "refreshing" and "less intense" relative to a cola, while still delivering a noticeable and satisfying carbonation experience to consumers who associate any sparkling drink with the need for a perceptible fizz. Lemon-lime sodas and tonic waters occupy this range commercially, and it is increasingly where innovative brands are finding product-market fit across multiple export markets simultaneously.

OEM Production Considerations: Cost, Complexity, and Flexibility

From a manufacturing standpoint, the choice between light and heavy carbonation is not just a marketing decision — it has direct implications for production line setup, quality control rigor, and packaging specifications. Laizhi Beverage's 50 flexible production lines are designed to handle the full commercial carbonation spectrum, from lightly sparkling teas to high-carbonation energy drinks, with HACCP-certified processes that ensure consistency across formats. Explore Laizhi's factory capabilities and certifications to understand what production precision looks like at scale.

Lightly carbonated products (1.5–2.5 vol) are generally more forgiving at the filling stage — lower internal pressure means less risk of seam stress, easier quality control, and broader compatibility with different packaging configurations. Heavily carbonated products (3.5–4.5 vol) require tighter temperature control at the carbonation and filling stages, more precise CO2 pressure management, and packaging that meets higher pressure ratings. The cost differential is modest at scale but can be meaningful for smaller launch quantities. For an OEM brand ordering its first run, specifying a moderate 2.8–3.2 vol target often gives the best balance between the consumer experience expected and the production precision required.

Which Format Should Your Brand Choose?

The question of which format "sells better" is ultimately a question about what "better" means for your specific business model. If your goal is maximum volume at mass-market price points in impulse-purchase channels with younger male consumers as your primary target, heavily carbonated energy drink or cola formats are more aligned with proven sales patterns. If your goal is premium margin, subscription or health-channel distribution, and brand loyalty from a wellness-oriented demographic, lightly carbonated functional beverages have the growth trajectory and pricing power to support a stronger long-term brand.

The most important insight for 2026 is that the two formats are not competing for the same consumer. They are different businesses with different economics, different channels, and different growth stories. The winning strategy is not picking the "better" format in the abstract — it's picking the format that is right for the consumer segment you have chosen to serve, then building your product brief, OEM specification, and distribution strategy around that decision. To discuss your OEM formulation requirements and explore which carbonation format fits your target market, browse the full Laizhi Beverage product portfolio to see the range of carbonated formats available for private label and custom development.

Frequently Asked Questions

Is lightly carbonated or heavily carbonated more popular globally?

By volume, heavily carbonated formats remain larger overall. By growth rate and consumer trend momentum, lightly carbonated is accelerating faster, particularly in high-income markets and among younger consumers. The global carbonated beverage market is approximately $590 billion, with traditional CSDs holding the majority share — but the premium and functional growth is concentrated in lower-carbonation formats.

Which format is easier to produce at small OEM quantities?

Lightly carbonated products are generally easier to manage at smaller MOQ runs due to lower pressure requirements and more forgiving filling tolerances. Both formats are commercially viable in OEM production, but high-carbonation products require stricter process controls that are easier to maintain consistently at higher production volumes.

Can I launch both formats under the same brand?

Yes, and many successful brands do exactly this — using light carbonation for their wellness or daily hydration SKU and high carbonation for their energy or indulgent line. The brand architecture challenge is ensuring the two formats feel coherent rather than contradictory. A wellness sparkling tea at 2.0 vol and an energy drink at 4.0 vol can coexist under the same brand if the packaging, positioning, and messaging clearly communicate the different use occasions. You can view the RTD product range for inspiration on how different carbonation formats can be managed across a single portfolio.

Do lightly carbonated drinks have a shorter shelf life?

Not inherently. Shelf life in canned beverages is primarily determined by can seam integrity, internal coating quality, and oxygen management at the filling stage — not CO2 volume alone. A well-filled, properly sealed lightly carbonated beverage in an aluminum can will maintain its carbonation level and flavor stability for 12–18 months, comparable to a heavily carbonated product produced under the same quality standards.