As of 2026, the global energy drinks market — valued at approximately USD 85 billion in 2025 and forecast to reach USD 158 billion by 2033 at a CAGR of 8.1% (Grand View Research) — is accelerating through a structural transition: the shift from synthetic to natural formulations. In 2026, this is no longer a trend on the horizon; it is the active buying brief for importers and OEM buyers across Southeast Asia, Europe, the Middle East, and North America.

As of 2026, the global energy drinks market — valued at approximately USD 85 billion in 2025 and forecast to reach USD 158 billion by 2033 at a CAGR of 8.1% (Grand View Research) — is accelerating through a structural transition: the shift from synthetic to natural formulations. In 2026, this is no longer a trend on the horizon; it is the active buying brief for importers and OEM buyers across Southeast Asia, Europe, the Middle East, and North America. Health-conscious consumers scrutinizing ingredient labels have moved from early adopters to mainstream, making clean-label formulation a commercial necessity rather than a premium option.

Key Takeaways

- Cans dominate energy drink packaging with 88.5% revenue share (2025 data), cementing aluminum as the default format heading into 2026 and beyond.

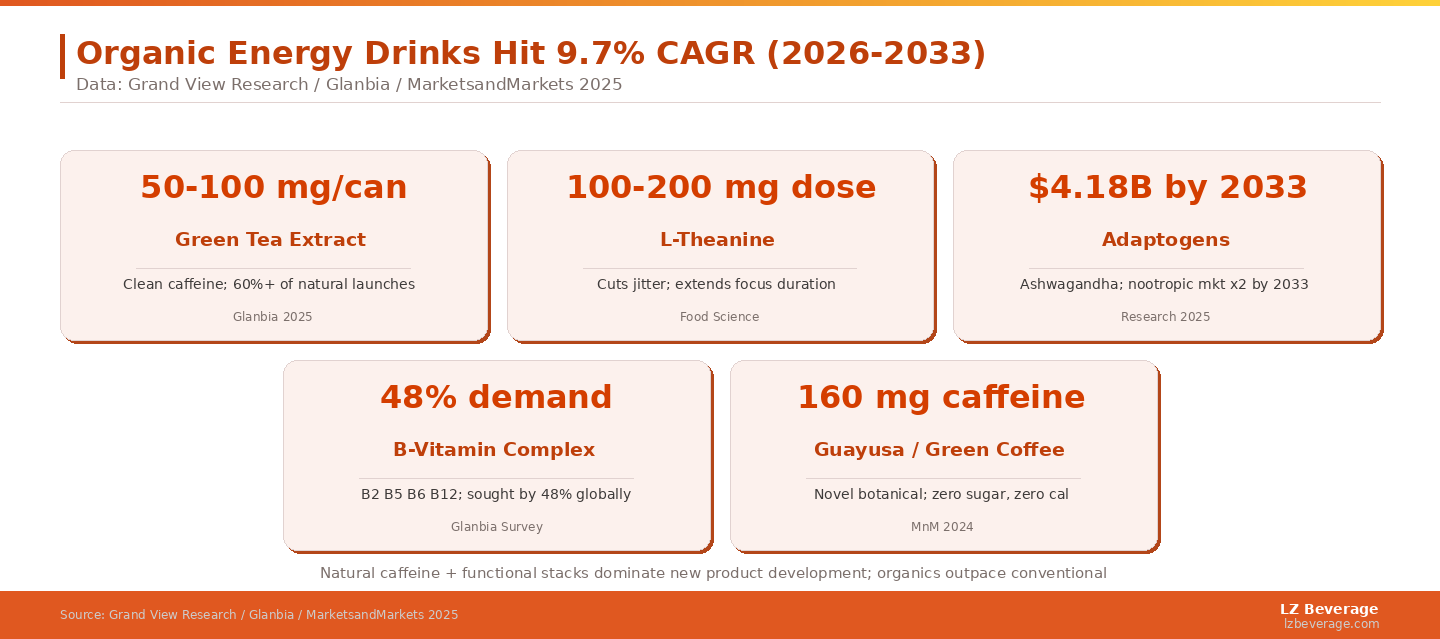

- The natural/organic energy drink segment is growing at 9.7% CAGR (2026–2033) — faster than the conventional segment — signaling a decisive shift in buyer demand.

- Five ingredients are leading the clean-label revolution: green tea extract, L-theanine, adaptogens, B-vitamin complex, and guayusa/green coffee.

- Asia-Pacific is the fastest-growing regional market at ~13% CAGR annually, creating strong demand for export-ready canned natural energy drinks.

- HACCP-certified OEM factories with flexible production lines are best positioned to serve brands entering the natural energy drink space.

Why Natural Energy Drinks in Cans Are Outpacing Traditional Formulas

The Can Advantage for Natural Formulas

Aluminum cans are not simply a packaging preference — they are a functional advantage for natural energy drink formulas. According to Market Data Forecast, a standard 250 ml energy drink can weighs only 13 grams while offering superior protection against light and oxygen degradation — precisely the conditions that degrade sensitive natural ingredients like taurine, B-vitamins, and botanical extracts. Cans are also 20% more transport-efficient than PET containers and 40% more efficient than glass bottles, according to data cited by Red Bull GmbH. For OEM brands targeting export markets in Africa, Southeast Asia, or the Middle East, this logistical advantage directly affects landed cost and shelf life.

Cans also lend natural energy drinks a perception premium. On shelf, aluminum communicates premium quality and sustainability — two attributes that resonate strongly with the wellness-oriented consumer who pays attention to ingredient sourcing. This is why custom canned energy drink development has become the primary brief for most OEM buyers seeking to enter the natural segment.

Market Signals OEM Brands Cannot Ignore

C-store energy drink dollar sales in the United States grew 10% in 2025 to more than USD 16 billion, according to C-Store Dive citing Circana data. More telling is the ingredient-level shift: 75% of energy drink consumers cite flavor as a top selection factor, but clean-label and no-artificial-sweetener options are rising as secondary filters across all demographics. Brands that launched with conventional formulas in 2020–2022 have been reformulating since 2025, and by 2026 the clean-label pivot is industry standard: synthetic sweeteners are being replaced with stevia or monk fruit, and artificial caffeine anhydrous is giving way to green tea or guayusa extract. For an OEM buyer placing orders for a new market, starting with a clean-label formula avoids a costly reformulation cycle 18 months after launch.

The natural and organic energy drink segment is projected to grow at 7.07% CAGR from 2024 to 2030, according to Research and Markets — faster than the broader market average of 5.9% in some forecasts. Africa is emerging as the fastest-growing volume market at 10.07% CAGR, driven by rapid urbanization and rising working-age populations. For factories with export certification, these are actionable procurement opportunities, not distant projections.

5 High-Demand Natural Ingredients Driving Canned Energy Drink Innovation

Understanding which ingredients are gaining traction — and why — is the most direct way to de-risk a new energy drink launch. The following five ingredients consistently appear across product development briefs, trade publication trend reports, and consumer research surveys for 2025–2026.

Green Tea and Green Coffee Extracts: The Clean Caffeine Foundation

Green tea extract and green coffee bean extract have become the primary caffeine sources for clean-label energy drinks. Glanbia Nutritionals research identifies both as the leading natural caffeine alternatives for fitness- and women-focused energy drinks. A single 250 ml can typically delivers 50–100 mg of caffeine from these sources, which aligns with the "smooth energy" positioning that differentiates natural products from high-stimulant conventional formulas. For OEM buyers, these extracts are now commodity-scale ingredients with stable supply chains, making them cost-effective anchors for any new natural formulation.

L-Theanine: The Anti-Jitter Pairing That Consumers Demand

L-theanine, an amino acid found naturally in tea leaves, is increasingly paired with caffeine in natural energy drink formulas. Its function is specific: it promotes relaxation without drowsiness while simultaneously reducing the anxiety and jitteriness that high-caffeine products can trigger. The result is what brands now market as "calm energy" or "clean focus" — an energy profile that appeals to working professionals, women, and wellness-oriented consumers who previously avoided energy drinks entirely. Typical dosages run 100–200 mg per can. From a formulation standpoint, L-theanine adds minimal flavor interference, making it an easy addition to virtually any flavor profile.

Adaptogens and Botanicals: From Niche to Mainstream

Ashwagandha, rhodiola, and other adaptogenic herbs have migrated from specialty supplements into mainstream canned energy drinks. The nootropic supplement market — which overlaps heavily with energy drink adaptogens — is projected to nearly double from USD 2.2 billion in 2023 to USD 4.18 billion by 2033, reflecting sustained consumer interest in stress-modulating ingredients. For OEM buyers, adaptogens serve a dual purpose: they deliver genuine functional benefits and provide marketing differentiation in a crowded SKU landscape. Ginseng, a long-established botanical in Asian markets, remains the most globally recognized adaptogen and should be considered a baseline ingredient for any energy drink targeting Asian, Middle Eastern, or health-focused European consumers.

B-Complex Vitamins: The Non-Negotiable Baseline

Across all market segments — conventional, natural, and functional — B-vitamins are essentially table stakes for energy drink formulations. According to Glanbia Nutritionals global consumer research, 48% of energy drink consumers worldwide express interest in B-vitamin enrichment. Vitamins B2, B5, B6, B7, and B12 are the most relevant due to their well-established roles in cellular energy metabolism. For OEM buyers, the practical implication is straightforward: any natural energy drink formula that omits B-vitamins will underperform on label value versus competing products. B-vitamins are low-cost, shelf-stable, and reinforce the natural-health positioning of the product.

Guayusa and Novel Botanicals: The Next Wave

Guayusa leaf — a caffeinated plant native to the Ecuadorian Amazon — has emerged as one of the most-discussed premium natural caffeine sources entering 2026. A November 2024 market entry by Oasis Energy Drink combined guayusa with green coffee to deliver 160 mg of natural caffeine per can at zero sugar and zero calories, according to MarketsandMarkets. This launch illustrates the direction of next-generation natural formulas: stacking two or more natural caffeine sources to achieve higher total caffeine without synthetic additives. OEM buyers exploring premium positioning in North American or European markets should include guayusa or yerba mate as options in their formulation brief.

OEM Opportunities: Building a Natural Energy Drink Line in Cans

Formulation Flexibility and Custom Caffeine Levels

One of the most critical capabilities to evaluate in an OEM manufacturing partner is formulation flexibility — specifically the ability to adjust caffeine levels, swap botanical sources, and modify sweetener systems across production runs. Different export markets carry different regulatory thresholds for caffeine content (the European Food Safety Authority sets 400 mg/day as the safe intake level for healthy adults), and what is compliant in the Gulf Cooperation Council may require reformulation for the EU. A capable OEM partner should support caffeine customization from 80 mg to 200 mg per can using natural sources, and provide documentation that supports regulatory submissions in target markets. Visiting a factory's production and quality assurance capabilities — including their R&D formulation records — before committing to a production run is essential due diligence.

What HACCP Certification Means for Natural Ingredient Sourcing

HACCP (Hazard Analysis and Critical Control Points) certification is not just a compliance checkbox — it is a signal that a factory operates with documented traceability systems for every incoming ingredient. For natural energy drinks, where ingredient authenticity and purity are marketing claims, this matters enormously. A HACCP-certified facility will track botanical extract origins, verify certificates of analysis from ingredient suppliers, and maintain batch records that can support label claims ("contains natural green tea caffeine") in target market audits. When evaluating OEM proposals for natural energy drink production, always request the factory's HACCP scope documentation and ask specifically which raw material categories fall within its HACCP program. You can read more about beverage certification standards and OEM selection criteria on our resource hub. You may also want to browse the full product range to understand which formats are available for private label programs.

From a practical standpoint, the OEM opportunity in natural canned energy drinks is most accessible for brands that can specify their target formulation tier (entry-level clean-label versus premium botanical), their target market's caffeine ceiling, and their packaging format upfront. Factories with integrated aluminum can supply and filling infrastructure — where both the can production and the beverage filling happen within the same supply chain — can reduce lead times by four to six weeks compared to split-sourcing arrangements. This integrated capability is particularly valuable for first-production runs, where timeline risk is highest. Explore custom energy drink OEM options to understand the scope of formulation and packaging configurations available for private label buyers.

Frequently Asked Questions

What caffeine level is standard in natural energy drinks in cans?

Most natural canned energy drinks target 80–160 mg of caffeine per 250 ml can, delivered through sources like green tea extract, green coffee bean extract, or guayusa. This range aligns with regulatory limits in major export markets and matches consumer expectations for a "smooth energy" profile. Brands positioning for the premium segment often combine two natural sources (e.g., green tea + guayusa) to reach 150–160 mg without synthetic caffeine anhydrous.

Can I get a private label natural energy drink in aluminum cans with a custom formula?

Yes. OEM manufacturers that operate integrated can filling facilities can accommodate fully custom natural formulas, including botanical extract selection, sweetener system (stevia, monk fruit, or no sweetener), and B-vitamin blends. The typical development process runs 8–12 weeks from formulation sign-off to first production samples. Buyers should request a pre-production sample before committing to a full container order.

What is the minimum order quantity for custom canned natural energy drinks?

MOQ varies significantly by manufacturer and production line configuration. For aluminum cans, most OEM facilities that support flexible production lines can accommodate starting orders of one to three 20-foot containers (approximately 20,000–50,000 cans per SKU). Buyers planning a multi-flavor launch across Southeast Asian or Middle Eastern markets often consolidate their initial order across two or three flavors to meet per-SKU MOQ thresholds while managing working capital. Discussing MOQ flexibility during the initial factory inquiry — before the formulation stage — saves significant time.

Which natural ingredients are most in demand in Asia-Pacific markets for energy drinks?

Asia-Pacific is the fastest-growing regional market at approximately 13% CAGR annually, and consumer preferences vary by sub-region. In Southeast Asia and China, ginseng and B-vitamins are the most recognized functional ingredients. In Japan and South Korea, L-theanine — already familiar from traditional tea culture — is a strong market-fit ingredient. In Australia and New Zealand, adaptogens like ashwagandha are gaining traction through fitness channels. Brands entering multiple Asia-Pacific markets simultaneously should prioritize ginseng and B-vitamin enrichment as their cross-market baseline, with regional flavor adaptations to drive local differentiation.