The global canned energy drink market is entering 2026 at full speed. According to Fortune Business Insights, the category is valued at USD 83.31 billion in 2026 and is forecast to reach USD 157.21 billion by 2034 at a CAGR of 8.26%. Behind those numbers lies a structural transformation: consumers are no longer buying a caffeine hit — they want a specific benefit, a clean label, and a format that fits their life.

The global canned energy drink market is entering 2026 at full speed. According to Fortune Business Insights, the category is valued at USD 83.31 billion in 2026 and is forecast to reach USD 157.21 billion by 2034 at a CAGR of 8.26%. Behind those numbers lies a structural transformation: consumers are no longer buying a caffeine hit — they want a specific benefit, a clean label, and a format that fits their life. For brand owners and OEM buyers evaluating product development or private label strategy this year, the following ten trends define where the market is heading and where the formulation and packaging opportunities lie.

Key Takeaways

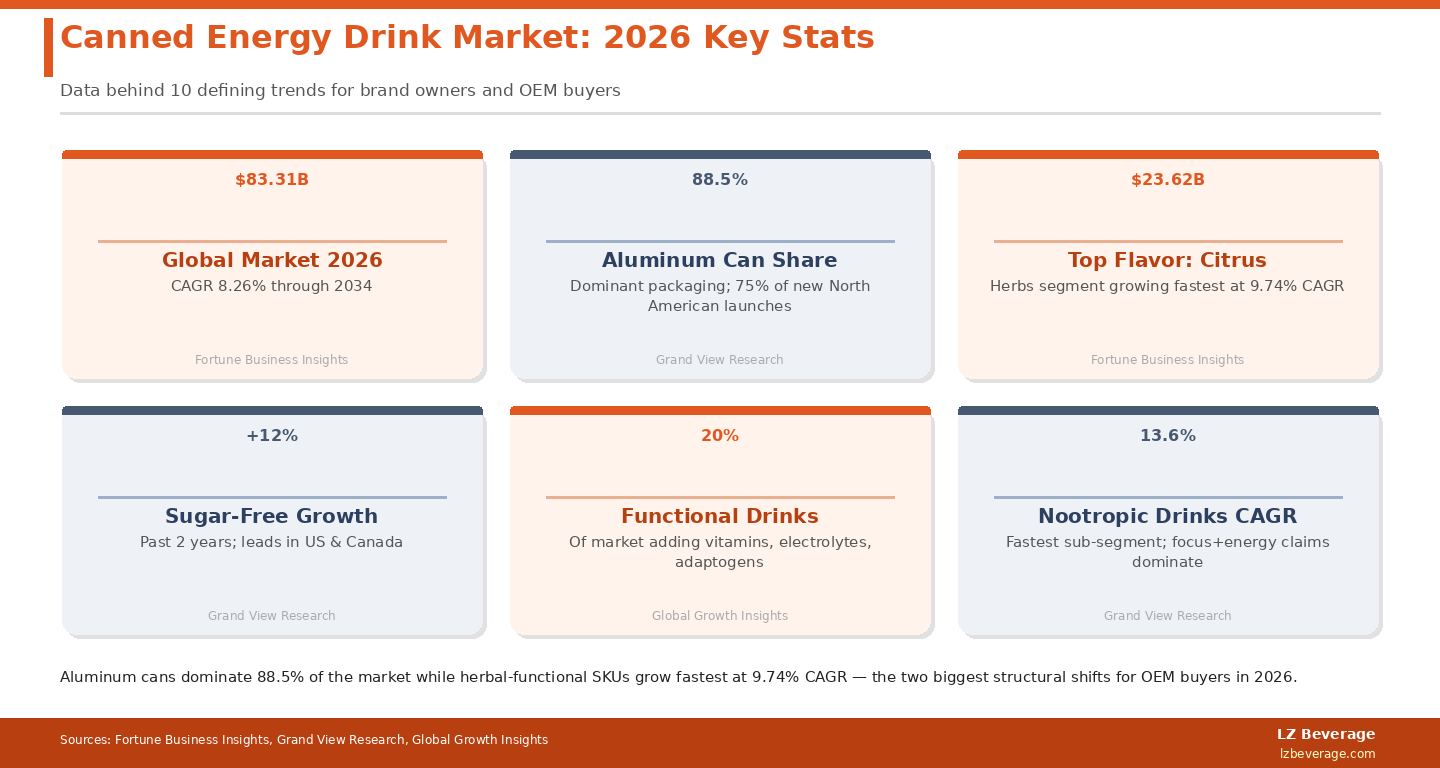

- Aluminum cans dominate 88.5% of energy drink packaging — sustainability and branding advantages are accelerating this further in 2026.

- Herbal and functional flavors are the fastest-growing segment, with a 9.74% CAGR outpacing the established citrus category.

- Sugar-free and low-sugar formulations have grown 12% in two years, driven by health-conscious purchasing in North America and Europe.

- Nootropic and adaptogen-fortified energy drinks are the fastest-growing sub-category at a 13.6% CAGR — a major OEM formulation opportunity.

- Gen Z is reshaping drinkability expectations: lighter mouthfeel, balanced flavors, and repeat-consumption palatability now matter more than peak caffeine content.

Trend 1: Functional Claims Are the New Standard, Not a Premium Feature

From "Energy" to Targeted Benefits

The broad "gives you energy" positioning that defined the 2010s is no longer sufficient. In 2026, consumers expect canned energy drinks to deliver specific, verifiable benefits: cognitive focus, hydration support, post-workout recovery, or mood stability. Straits Research reports the global market reached USD 114.74 billion in 2026, driven significantly by functional ingredient innovation — with electrolytes, adaptogens, and nootropics now appearing alongside traditional caffeine and taurine in mainstream formulations. For OEM brands entering or expanding in this space, the functional claim is the product brief, not an afterthought.

Benefit Stacking Becomes the Differentiation Strategy

According to BevSource's 2026 beverage trend analysis, "benefit stacking" — combining energy with gut health, hydration, or immunity in a single SKU — is becoming a standard innovation framework, provided that one benefit remains clearly primary. Brands formulating for the OEM market should plan their functional architecture before selecting ingredient suppliers: the regulatory compliance and label design implications differ significantly between a "hydration + energy" claim versus a "nootropic focus + energy" claim.

Trend 2: Sugar-Free and Low-Sugar Dominate New Launches

Health Consciousness Is Reshaping the Formulation Brief

The shift away from high-sugar energy drinks is no longer trend language — it is category math. Grand View Research confirms the sugar-free segment has grown approximately 12% over the past two years, with sugar-free options leading purchasing decisions in the US and Canada. The organic sub-segment is projected to grow at the fastest CAGR of 9.7% through 2033, driven by consumers seeking formulas free from artificial sweeteners and synthetic additives. OEM manufacturers with proven zero-sugar sweetener blends — using stevia, erythritol, or monk fruit — are increasingly differentiated in RFQ processes.

Plant-Based Sweetener Innovation

Alongside sweetener reduction, the origin of sweetening agents matters. Plant-based sweeteners from agave, coconut sugar, and monk fruit are gaining shelf space not just for calorie reduction but for clean-label positioning. For brands targeting health-food retail channels or premium convenience store placement, specifying a named plant-based sweetener in the ingredient list is now a procurement requirement, not just a marketing preference.

Trend 3: Exotic and Functional Flavor Innovation

Citrus Holds, But Herbals Are the Growth Engine

Citrus remains the largest flavor segment at USD 23.62 billion in 2025, according to Fortune Business Insights, but it is the herbal segment that is growing fastest — at a projected 9.74% CAGR through 2034. Mango, strawberry, watermelon, and berry account for the highest volume of new launches, while passion fruit, peach, and mushroom-based profiles are gaining commercial significance. For OEM clients evaluating flavor SKU strategy, a core citrus/berry lineup supplemented by two to three herbal-botanical SKUs (yuzu, lychee, elderflower) offers the most balanced risk-reward position in 2026.

Swicy: The Emerging Flavor Frontier

The "swicy" (sweet + spicy) trend — documented by BevSource as moving toward layered profiles like mango habanero and guava jalapeño — represents one of the higher-risk, higher-reward formulation bets of 2026. Capsaicin levels must be calibrated carefully for the carbonated format, where heat perception is amplified. For brands willing to invest in flavor development and consumer testing, a well-executed swicy energy drink commands premium retail pricing and strong social media traction.

Trend 4: Nootropics and Adaptogens Enter the Mass Market

Cognitive Enhancement Moves From Supplement Aisle to Beverage Shelf

The nootropic and cognitive health drinks market is growing at a 13.6% CAGR according to Grand View Research, driven by consumer demand for focus enhancement without the jitteriness of traditional high-caffeine formulas. Ingredients like L-theanine (paired with caffeine for a "smooth energy" profile), lion's mane mushroom, citicoline, and ashwagandha are being added to canned energy drink formulations by both established brands and emerging labels. A March 2026 launch from Happy Panda — featuring Cognizin Citicoline, natural caffeine, and electrolytes — sold out half its initial stock within one month, illustrating the velocity potential of a well-positioned nootropic energy drink. For custom energy drink formulation clients, nootropic-grade ingredient sourcing and dosage transparency are the two critical success factors.

Adaptogen Standardization Becomes an OEM Competency

While adaptogens like ashwagandha and ginseng have been in the market for years, 2026 marks the point where standardized extract specifications — defining KSM-66 ashwagandha vs. generic ashwagandha root powder, for example — are becoming part of OEM buyer briefs. Brands that can verify adaptogen provenance and potency on their CoA documentation are able to access premium retail channels that require substantiated functional claims.

Trend 5: Gen Z Drinkability Standards Are Raising the Flavor Bar

Sensory Fatigue Is the New Consumer Enemy

Research from FoodNavigator Asia published in April 2026 documents a fundamental shift in Gen Z purchasing behavior: energy drink selection increasingly centers on drinkability over stimulation intensity. Flavor balance, lighter mouthfeel, and clean finish — characteristics that allow sustained consumption during gaming sessions, study periods, or long workdays — are now primary selection criteria. Brands optimizing for repeat purchase (rather than first-trial novelty) need formulation briefs that specify sensory fatigue thresholds, not just caffeine content.

Trend 6: Aluminum Cans Consolidate as the Dominant Format

90%+ Market Coverage and Growing

Aluminum cans account for over 90% of energy drink packaging globally, according to Packaging Dive's February 2026 analysis. The can's functional advantages — portability, rapid chillability, light-proof barrier, and neutral taste transmission — combine with its recyclability story to make it effectively the default format for new energy drink launches. Beverage Industry Magazine reports that 75% of all new beverage launches in North America now use aluminum cans — more than double the rate of five years ago. For OEM buyers, this means that working with a manufacturer offering integrated aluminum sourcing and filling — rather than procuring the two separately — materially reduces logistics cost and lead time. At Laizhi Beverage, aluminum can production and filling lines operate on the same site, enabling a streamlined one-stop OEM/ODM workflow.

Trend 7: Seasonal and Limited-Edition Releases Drive Incremental Revenue

Exclusivity as a Retail Strategy

Seasonal and limited-edition claims in the energy drink category are growing at a 12% CAGR, making them one of the highest-velocity promotional mechanics in the sector. Digital printing technology on aluminum cans has lowered the MOQ barrier for limited runs, allowing brands of all sizes to execute seasonal campaigns without committing to full production volumes. The retail logic is straightforward: limited editions create urgency, drive trial among fence-sitters, and generate social media content without requiring a permanent SKU addition. For OEM clients evaluating their annual new product introduction (NPI) calendar, building two to three limited-edition campaigns alongside a core lineup is now standard planning practice.

Trend 8: Caffeine Customization by Daypart and Occasion

The Spectrum From 80mg to 300mg+ Is Now Commercially Viable

Energy drink manufacturers are increasingly customizing caffeine levels by target occasion rather than applying a single dose across their lineup. IndexBox reports that while 75% of consumers cite flavor as the top purchase driver, caffeine dosage customization is the most actively discussed innovation area among energy drink manufacturers heading into 2026. Morning formulas at 80–120mg, afternoon focus variants at 150–200mg, and pre-workout formulas at 250–300mg represent distinct positioning opportunities — each with different regulatory consideration thresholds depending on the target market.

Trend 9: Clean Label and Ingredient Transparency

Label Readability Is Now a Purchase Conversion Factor

In the US and Canada, 29% of consumers actively check ingredients and labels before purchasing energy drinks, according to consumer panel data cited by market research sources tracking the sector. The clean label trend in energy beverages means shorter ingredient lists, named natural caffeine sources (green coffee extract, green tea, guarana, yerba mate), and no artificial colors or synthetic preservatives. For brands building a private label energy drink from the ground up, ingredient list architecture should be finalized before formulation begins — the label is a marketing document as much as a regulatory requirement.

Trend 10: Asia-Pacific Emerges as the Key Growth Market

OEM Opportunity: Formulation for Local Taste Profiles

While North America dominates current market value at approximately 37–39% global share, Asia-Pacific is the fastest-growing region for canned energy drinks — driven by urbanization, rising middle-class consumption, and expanding modern retail infrastructure. China's energy drink market alone is projected to exceed USD 8 billion by 2034. Southeast Asian consumers show distinct taste preferences (lighter sweetness, lychee and yuzu profiles, lower caffeine tolerance) compared to North American buyers. OEM manufacturers with Asia-Pacific export experience — including HACCP certification, multilingual labeling capability, and compliance with local food safety standards — are positioned to capture this growth wave ahead of brands still relying on single-market formulations.

| Trend |

OEM Formulation Priority |

Market Signal |

| Functional Claims |

Electrolytes, adaptogens, nootropics |

+18% new product launches with functional ingredients |

| Sugar Reduction |

Plant-based sweeteners, zero-sugar base |

+12% growth in 2 years; 9.7% organic CAGR |

| Flavor Innovation |

Herbal-botanical, swicy, exotic fruits |

Herbs segment CAGR 9.74% — fastest in flavor category |

| Aluminum Cans |

Integrated sourcing + filling |

88.5% market share; 90%+ of energy drink packaging |

| Limited Editions |

Low-MOQ digital print runs |

Seasonal claims growing at 12% CAGR |

| Asia-Pacific Expansion |

Local taste profiles, export compliance |

China projected >USD 8B by 2034 |

Frequently Asked Questions

What is the biggest canned energy drink trend in 2026?

The shift toward functional claims beyond basic energy is the defining trend of 2026. Consumers now expect energy drinks to deliver specific benefits — cognitive focus, hydration, recovery, or mood support — making functional ingredient selection the core differentiator in product development. Sugar-free formulations and nootropic ingredients are the two fastest-growing formulation categories within this broader shift.

Which flavors are growing fastest in canned energy drinks?

Herbal and botanical flavors are growing fastest, with a projected 9.74% CAGR according to Fortune Business Insights — outpacing even the established citrus segment. Fruit flavors (mango, watermelon, passion fruit, lychee) continue to account for 82% of new launches, but brands seeking differentiation are layering botanical notes (yuzu, elderflower, hibiscus) on top of fruit base profiles to create distinctive market positioning.

What can sizes are trending in 2026?

Smaller formats are gaining traction: the 8.4 oz (250ml) can is becoming standard rather than niche, driven by brands targeting lower caffeine dosages and broader daypart appeal. The 16 oz (500ml) format remains dominant in the sports and hardcore gamer segments. For OEM clients building a product lineup, offering the same core formula across 250ml and 330ml SKUs is the standard approach to cover both convenience-store impulse and multipack retail.

How important is aluminum can sustainability for energy drink brands in 2026?

Sustainability credentials are now a purchasing factor for a significant portion of energy drink consumers, particularly in European and North American markets. Aluminum's infinite recyclability is the most defensible packaging sustainability claim in the beverage sector — and brands are actively incorporating it into label design and marketing communications. For OEM buyers, working with a manufacturer using ASI-certified aluminum is a procurement advantage in markets with Extended Producer Responsibility regulations.

Is the energy drink market still growing in 2026?

Yes, and robustly. Multiple market research sources place the global energy drink market at USD 83–115 billion in 2026 depending on scope methodology, with CAGRs ranging from 6.8% to 8.26% through 2034. The category is structurally supported by urbanization, rising fitness participation, expanding convenience retail in Asia-Pacific and the Middle East, and continuous product innovation. For brand owners evaluating OEM partnership, the market fundamentals favor investment in new SKU development across functional, low-sugar, and flavor-forward positions. Learn more about beverage industry trends and OEM guides at Laizhi Beverage's resource center.