Sugar is the single most regulated ingredient in the global carbonated beverage industry. Over 100 countries and territories now operate some form of sugar-sweetened beverage tax, according to the World Health Organization's 2025 Global Report on SSB Taxes, and the number continues to grow. At the same time, consumer attitudes are shifting: Innova Market Insights reports that 72% of global consumers are actively limiting their sugar consumption.

Sugar is the single most regulated ingredient in the global carbonated beverage industry. Over 100 countries and territories now operate some form of sugar-sweetened beverage tax, according to the World Health Organization's 2025 Global Report on SSB Taxes, and the number continues to grow. At the same time, consumer attitudes are shifting: Innova Market Insights reports that 72% of global consumers are actively limiting their sugar consumption. For brand owners developing carbonated canned drinks, sugar is no longer just a flavor variable — it is a strategic decision that directly affects production cost, retail pricing, market access, and regulatory compliance across every target geography.

Key Takeaways

- A standard full-sugar cola contains approximately 10–11 g sugar per 100 mL, delivering 33–39 g per 330 mL can — well above WHO's recommended daily free sugar guideline of 25 g.

- The UK's tiered Soft Drinks Industry Levy (at 8 g/100 mL threshold) has become the de facto global benchmark for export formulation decisions; European markets are following with their own tiered structures.

- Four formulation tiers exist — full sugar, reduced sugar, low sugar, and zero sugar — each with distinct taste, stability, cost, and regulatory implications that vary by market.

- Choosing the right sugar level is not purely a health decision: it is a distribution strategy, a pricing decision, and increasingly a tariff avoidance calculation.

Baseline: What Sugar Levels Look Like in Commercial Carbonated Drinks

The Standard Full-Sugar Formula

In a traditional full-sugar cola format, sucrose or high-fructose corn syrup (HFCS) is typically dosed at 10–11 g per 100 mL — meaning a standard 330 mL aluminum can delivers approximately 33–39 g of total sugar. A comparative study published in PubMed Central analyzing the same branded products across China, the UK, and the USA found that Coca-Cola Classic ranged from 6.6 g/100 mL (UK, post-SDIL) to 11.0 g/100 mL (USA), demonstrating how regulatory pressure directly reshapes the same product's formulation across geographies. As the Harvard T.H. Chan School of Public Health's Nutrition Source notes, the American Heart Association recommends a maximum of 25 g of added sugar per day for women and 36 g for men — meaning a single can of standard cola essentially reaches or exceeds the recommended daily limit in one serving.

Fruit-flavored carbonated drinks (orange, lemon-lime, grape) tend to cluster in the 9–12 g/100 mL range, slightly higher than cola in some formulations due to the need to balance stronger organic acid contributions. Energy drinks, which also carry a caffeine functional payload, typically target 10–13 g/100 mL in full-sugar formats. Lightly carbonated fruit sodas and sparkling teas often come in at 6–9 g/100 mL — a naturally lower-sugar tier that also positions better against growing wellness consumer expectations.

What Sugar Actually Does in a Carbonated Formula

Sugar performs three simultaneous roles in a carbonated canned drink that are easy to underestimate when making the decision to reduce it. First, it provides sweetness intensity and the characteristic flavor "body" — the full, slightly viscous mouthfeel that many consumers unconsciously associate with quality. Second, it interacts with the acidity from CO2 and added acidulants to create the sweet-sour balance that defines refreshment in this category; remove the sugar without adjusting the acid balance and the drink tastes aggressively sour. Third, sugar contributes to the physical stability of flavor compounds in solution, helping certain volatile esters and fruit notes stay in suspension rather than drifting or degrading over shelf life. These three functions all need to be addressed separately when reformulating to lower sugar levels — which is why sugar reduction is technically complex, not just a matter of reducing one ingredient's dosage.

The Global Sugar Tax Landscape: What Your Target Market Costs

As of 2026, the Tax Foundation reports that at least 17 European countries levy some form of SSB tax, with more markets implementing tiered structures that actively incentivize brands to reformulate below specific thresholds. Understanding this landscape is not optional for any brand with export ambitions.

The UK: The Benchmark Threshold System

The UK's Soft Drinks Industry Levy (SDIL), implemented in 2018, operates on two tiers: drinks with 5–8 g sugar/100 mL face a lower levy rate, while drinks at or above 8 g/100 mL face the higher rate. This threshold system has had a measurable reformulation impact — a 2025 Cambridge University study found the tax reduced roughly 6,600 calories per year per UK resident, with 80% of that reduction attributable to manufacturer reformulation rather than consumer behavior change alone. The 8 g/100 mL threshold has effectively become an industry benchmark: brands targeting UK market entry routinely design their core formula to land below this level, producing a product that also performs well across other European tiered regimes.

Europe: An Expanding Tiered Regime

France, Ireland, and Portugal all operate tiered excise systems that rise with sugar content, and Estonia, Lithuania, and Italy are implementing new SSB taxes in 2026, expanding the European regulatory environment considerably. Lithuania's new structure, for example, taxes drinks at ≥8 g sugar/100 mL at approximately €0.21/L, while drinks below 8 g face €0.074/L — a near 3× cost differential that directly affects product economics at export scale. For a brand owner shipping 500,000 cans to European markets, the difference between a formula at 7.9 g/100 mL versus 8.1 g/100 mL can represent a material cost at the container level.

Middle East: Volume Market with Growing Regulatory Pressure

The GCC countries — Saudi Arabia, UAE, Bahrain, Qatar, Oman, and Kuwait — introduced a 50% ad valorem excise tax on carbonated drinks and a 100% tax on energy drinks across the region from 2017–2019. The tax applies to all carbonated beverages regardless of sugar content in most of these markets, meaning a sugar reduction strategy alone does not provide a tax exemption benefit. However, several GCC markets are under active discussion about tiered sugar-based structures aligned with WHO guidance, and the general direction of travel is toward stricter nutritional standards. For OEM brands targeting the Middle East, the more pressing formulation decisions today are HALAL compliance and labeling accuracy rather than sugar tier, but this is a rapidly evolving regulatory environment worth monitoring closely.

Southeast Asia: High Volume, Emerging Regulation

Markets like Malaysia, Thailand, Vietnam, and Indonesia are implementing or considering SSB taxes at different speeds. Malaysia introduced a tiered beverage tax in 2019 (drinks ≥5 g/100 mL), making it one of the first Southeast Asian markets with a sugar-threshold levy. The Philippines, Singapore, and others are at various stages of consultation and implementation. Consumer taste preferences in many Southeast Asian markets continue to favor sweeter flavor profiles compared to Western markets — but the regulatory direction is clearly toward restriction, and export brands building for long-term Southeast Asian distribution need a formula that can perform commercially at 8–10 g/100 mL today while being reformulatable below 5–8 g within a two-to-three year window. Laizhi's flexible OEM production infrastructure is built to support exactly this kind of staged reformulation without requiring a full production line retool between batches.

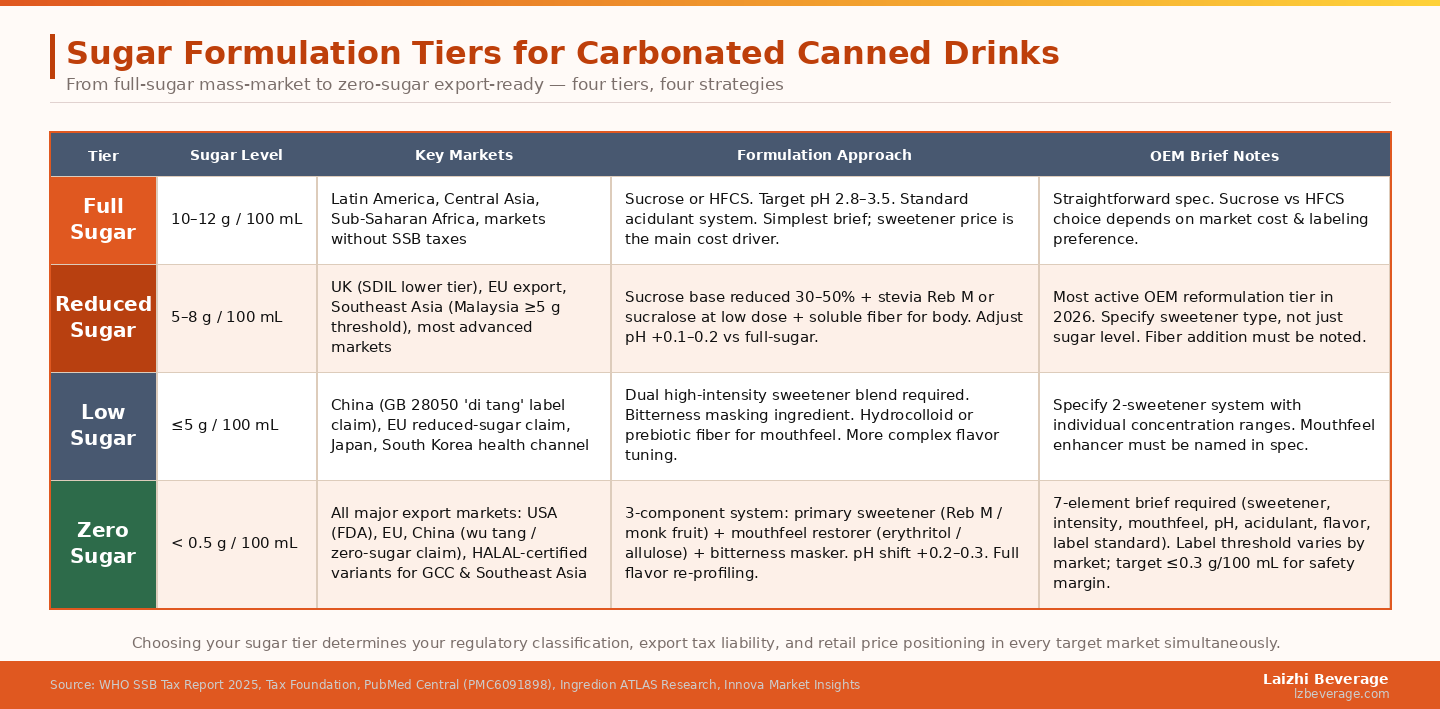

The Four Formulation Tiers: A Brand Owner's Reference

Tier 1: Full Sugar (10–12 g/100 mL)

Full-sugar formulations remain the dominant format in markets without active SSB taxes, and they retain clear taste advantages — the richest mouthfeel, strongest flavor stability, and least formulation complexity. In markets where the regulatory environment is stable and consumer demand for sugar-heavy formats persists (parts of Latin America, Central Asia, sub-Saharan Africa), full-sugar formulations remain commercially optimal. The OEM brief for this tier is the most straightforward: specify sucrose or HFCS concentration, target pH and carbonation level, and validate against the shelf-life target. The primary production cost driver is sweetener price, which varies considerably between sucrose (from cane or beet) and HFCS depending on regional availability and trade conditions.

Tier 2: Reduced Sugar (5–8 g/100 mL)

The reduced-sugar tier is where most export-oriented reformulation activity is concentrated in 2026. Products formulated in this range clear the UK SDIL lower threshold, qualify for favorable tax treatment in France, Ireland, and Lithuania, and avoid the top tier of most other European and some Asian levy structures. The formulation challenge in this range is filling the mouthfeel and sweetness gap left by the 30–50% sugar reduction without introducing off-notes. The most effective strategies combine a modest high-intensity sweetener addition (typically stevia Reb M or sucralose at low doses) to restore peak sweetness intensity, fiber addition (such as soluble corn fiber or inulin) to restore body and mouthfeel, and minor flavor system adjustment to compensate for the slightly flatter mid-palate sensation that reduced sugar creates. According to Ingredion's proprietary consumer research, 45% of shoppers are primarily motivated by nutrition and wellness, and 14% will pay up to 30% more for no-added-sugar claims — making the reduced-sugar tier a credible commercial upgrade rather than a cost-reduction measure.

Tier 3: Low Sugar (≤5 g/100 mL)

The low-sugar tier is typically defined by the Chinese national standard (≤5 g/100 mL for "低糖" claims) and closely mirrors several other Asian and European labeling thresholds for reduced-sugar claims. Formulating reliably at this level requires a more substantial sweetener system — typically a blend of two or more high-intensity sweeteners to cover different points of the sweetness curve and minimize the lingering aftertaste that single-sweetener systems often produce at high replacement rates. Flavor masking ingredients become important at this tier to cover the slight bitterness that most high-intensity sweeteners introduce at the concentrations needed to fully replace 5+ g/100 mL of sugar. This is also the tier where mouthfeel enhancement through hydrocolloids or beverage fibers becomes non-optional — consumers perceive low-sugar drinks as "watery" without this structural compensation.

Tier 4: Zero Sugar (<0.5 g/100 mL)

Zero-sugar formulation is covered in depth in the companion article on sweetener-based OEM products. From a sugar content perspective, the key point for brand owners at this tier is label compliance: the "zero sugar" or "sugar-free" claim definition varies by market. FDA (USA) defines zero sugar as <0.5 g per reference amount, EU regulations follow similar thresholds, while Chinese standards apply "无糖" classification for <0.5 g/100 mL. A formulation that meets zero-sugar thresholds in all three jurisdictions simultaneously is commercially achievable but requires careful co-formulation of sweetener selection and flavor system. The Laizhi energy drink OEM line supports zero-sugar formulation across both full-caffeine and reduced-caffeine energy drink formats.

Practical OEM Brief Considerations for Sugar Specification

When briefing an OEM manufacturer on sugar content, brand owners frequently under-specify in ways that create expensive reformulation cycles. A complete sugar specification includes the target sugar level in g/100 mL, the acceptable tolerance (±0.3 g/100 mL is typical for commercial production), the approved sweetener system (sucrose, HFCS, sucrose/stevia blend — each produces different sensory and stability outcomes), and any market-specific labeling requirements that constrain ingredient choices. For example, stevia is approved in the EU under specific E-number designations (E960) and in the USA under GRAS status, but regulatory status varies across Southeast Asian and Middle Eastern markets and should be confirmed before selecting it as the primary sweetener in an export product.

The interaction between sugar level and pH specification is also critical to communicate: a formula targeting 7 g/100 mL sugar at pH 3.2 will taste and perform differently from one at pH 3.8, even if the sugar level is identical. Refreshment perception, flavor brightness, and microbial stability all shift meaningfully across this range. The complete picture for any OEM brief is sugar level + sweetener type + pH target + carbonation level — four variables that must be specified together to produce a first-sample product that lands in the right taste quadrant. For brands ready to start developing a custom carbonated canned drink, the Laizhi Beverage team supports full formulation briefing from concept to first sample.

Frequently Asked Questions

What is the UK sugar tax threshold for carbonated drinks?

The UK Soft Drinks Industry Levy (SDIL) has two tiers: the lower levy applies to drinks with 5–8 g sugar per 100 mL, and the higher levy applies to drinks at or above 8 g per 100 mL. Drinks with less than 5 g/100 mL of sugar are exempt. This threshold has effectively become the global benchmark for export-oriented reformulation strategy.

Is sugar reduction in carbonated drinks technically complex?

Yes — and this is commonly underestimated. Sugar performs three functions simultaneously: sweetness intensity, flavor body and mouthfeel, and physical stability of volatile flavor compounds. Reducing it without addressing all three typically produces a product that is thinner, flatter, and less stable than the original. Successful reduced-sugar formulation requires a combination of high-intensity sweeteners, mouthfeel enhancement ingredients, and flavor system adjustment to fully compensate.

Does a lower-sugar formula cost more to produce?

At the ingredient level, high-intensity sweeteners cost more per kilogram than bulk sugar, but the volumes used are dramatically lower due to their sweetness intensity — so the net cost impact is often close to parity. The larger cost factor is typically the additional formulation development work to achieve a first-sample product that tastes right, and in some markets, the higher retail price premium that a reduced-sugar or zero-sugar claim supports. Research cited by Ingredion suggests 14% of consumers will pay up to 30% more for health-forward sugar claims, indicating that the price premium available in many markets more than offsets the modest formulation cost increase.

Which markets currently have the highest sugar tax rates on carbonated drinks?

Among global markets, Norway levied one of the highest SSB excise duties before rolling back its tax. Among active markets in 2026, France, Ireland, the UK, and Portugal operate structured tiered systems with meaningful tax differentials between high-sugar and low-sugar formulations. In the GCC, the 50% ad valorem structure applies to all carbonated drinks regardless of sugar content, making it a flat levy rather than an incentive for reformulation.

Can the same formula be used across Europe, the Middle East, and Southeast Asia?

A single formula targeting 6–7 g sugar/100 mL with a stevia/sucrose blend can often perform across these geographies from a regulatory standpoint, but taste profiling may need regional calibration — Southeast Asian consumers in particular typically expect a sweeter, fuller flavor profile than European consumers at the same nominal sugar level. Working with an OEM partner who understands regional consumer taste benchmarks is important for an export brand strategy that covers multiple geographies simultaneously.